You are currently browsing the category archive for the ‘Economy’ category.

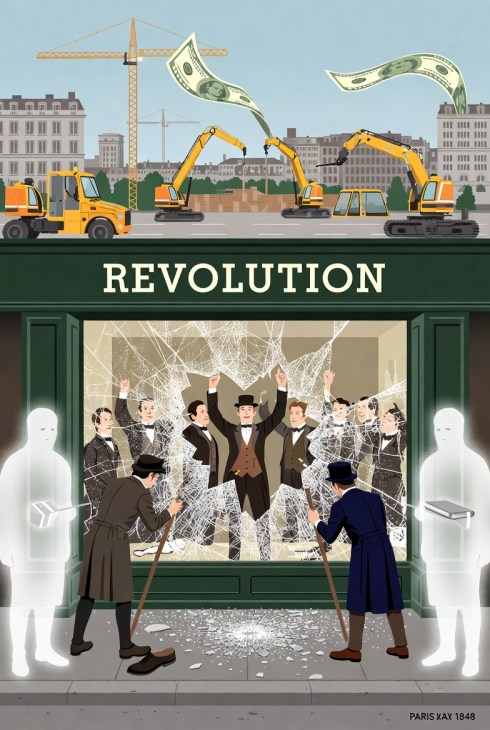

The ‘Broken Window’ parable has lasted because the mistake it identifies is permanent. People keep confusing motion with wealth.

A shop window gets smashed. The glazier benefits. He is paid to replace it. Money changes hands. Work is created. Onlookers reassure themselves that the damage at least “helped somebody.” Bastiat’s point is that this is where bad economic reasoning begins. The shopkeeper must now spend money restoring what he already had instead of buying something new, improving his business, saving, or investing. The glazier gains work. The shopkeeper loses options. Society ends up with a replaced window instead of a replaced window plus whatever else might have been created. That is not growth. It is recovery from loss.

In That Which Is Seen, and That Which Is Not Seen, published in 1850, Bastiat gave this simple error its enduring form. The visible effect is easy to grasp: the glazier gets income, then spends it elsewhere, and activity ripples outward. But the visible beneficiary is only half the story. What disappears from view are the unrealized alternatives: the suit never bought, the tool never purchased, the apprentice never hired, the expansion never attempted. The fallacy survives because the gain is concrete and public while the loss is dispersed and hypothetical. One can be pointed to. The other must be reasoned out.

“People keep confusing motion with wealth. Visible activity is easy to celebrate. The wealth that never came into being is harder to see, and easier to ignore.”

That is why the broken window is not really about vandalism. It is about how easily public argument stops at the first visible effect and calls the matter settled. Once you see that, a great deal of modern economic rhetoric starts to look less like analysis than stagecraft.

The pattern is familiar in debates over stimulus spending. Governments announce major spending packages. The public is shown crews on worksites, contracts being signed, jobs being counted, funds “flowing into the economy.” The imagery is always immediate and flattering. Something is happening. Therefore something good must be happening.

But visible activity is not the same thing as net wealth creation. Government does not create resources from nothing. It taxes them away, borrows them away, or inflates them away. In each case, resources are redirected from other possible uses. The serious question is not whether public spending produces measurable effects. Of course it does. The serious question is whether those resources would have created more value had they remained in private hands, guided by price signals, local knowledge, and voluntary choice rather than political allocation.

That is where the unseen side of the ledger matters. We see the bridge. We do not see the private investment that never happened because capital was drawn elsewhere. We see the subsidized payroll. We do not see the household purchasing power weakened by inflation. We see the grant recipient. We do not see the startup that never secured financing, or the consumer demand that was blunted by higher taxes or debt service. Public spending can make its beneficiaries highly visible while leaving its displaced alternatives diffuse and mostly invisible. That is politically useful, but analytically weak.

The usual reply is that recessions change the equation. When labour is idle, capital is underused, and private demand collapses, government spending may mobilize resources that would otherwise sit dormant. That is the strongest counterargument, and it should be taken seriously. A deep recession is not the same as a fully employed economy. Slack matters. Timing matters. Liquidity panics matter. A blanket denial of all countercyclical policy is cruder than Bastiat’s actual insight deserves.

But this does not rescue the broken window logic from criticism because it does not actually answer it. Even in a downturn, the central question remains comparative: compared to what? If the claim is that temporary public spending can stabilize demand under exceptional conditions, that is at least a serious argument. But it is not the same argument as saying that destruction creates prosperity, or that politically directed spending is wealth in itself. It still matters what is being funded, how efficiently it is administered, what incentives it creates, and whether the spending is genuinely using idle resources or merely displacing better uses that are harder to measure in real time.

“Replacement is not creation. Redirection is not prosperity. A society does not become richer by repairing destruction and calling the bustle growth.”

That distinction matters because bad arguments often smuggle themselves in under good intentions. A narrow case for emergency stabilization can turn into a permanent political habit of treating state spending as inherently productive. Once that shift happens, Bastiat’s warning reasserts itself in full. Replacement is still not creation. Redirection is still not spontaneous enrichment. Measured output can rise while underlying wealth formation weakens.

The same mistake appears after natural disasters and during wartime booms. After a hurricane, people say rebuilding will “boost the economy.” During war, people point to full factories and rising production figures. But rebuilding what was destroyed is not the same as becoming richer. Producing goods for destruction is not the same as expanding civilian prosperity. These events may generate employment, contracts, and output. They do not erase the prior loss. The relevant comparison is not between disaster and inactivity. It is between the world after destruction and the world in which the destruction never occurred.

That is what makes Bastiat’s lesson both obvious and routinely ignored. Visible motion is emotionally persuasive. A ribbon-cutting is easier to celebrate than an opportunity cost. A government announcement is easier to narrate than a private investment that never happened. Political systems are structurally biased toward what can be displayed, counted, branded, and claimed. The unseen has no ceremony attached to it. It leaves no plaque.

So the broken window fallacy endures not because the logic is hard, but because the discipline is hard. It requires people to keep asking the next question after the applause line. Jobs doing what? Spending on what? At whose expense? Relative to which forgone alternative? In a free economy, resources are scarce and choices are real. To pretend otherwise because spending is visible is to confuse accounting entries with prosperity.

Bastiat’s point remains devastating because it cuts through so much noise. Destruction does not enrich. Replacement does not add net wealth. Spending is not identical with prosperity. A society becomes richer when it creates new value, lowers costs, improves production, expands choice, and allows people to direct resources toward ends they actually value. It becomes poorer when it burns wealth, redirects capital by force, and congratulates itself for the bustle that follows.

That was true in Bastiat’s time. It is true now. The forms get larger, the numbers get bigger, and the rhetoric gets smoother, but the underlying mistake does not change. The glazier is still real. So is the window. So is everything we never got because we mistook repair, diversion, and visible activity for growth.

References

Bastiat, Frédéric. “What Is Seen and What Is Not Seen.” Online Library of Liberty.

https://oll.libertyfund.org/pages/wswns

Bastiat, Frédéric. “That Which Is Seen, and That Which Is Not Seen.”

https://bastiat.org/en/twisatwins.html

Bastiat, Frédéric. “Chapter 1: What Is Seen and What Is Not Seen.” Econlib.

Encyclopaedia Britannica. “Frédéric Bastiat.”

https://www.britannica.com/money/Frederic-Bastiat

Cullen, Joseph A., and Roger H. Gordon. “Taxes and Wartime Mobilization in the U.S. Economy: World War II as a Natural Experiment.” NBER Working Paper 12801.

Garin, Andy. “The Wartime Origins of Industry Location and Economic Mobility in the United States.” NBER Working Paper 33418.

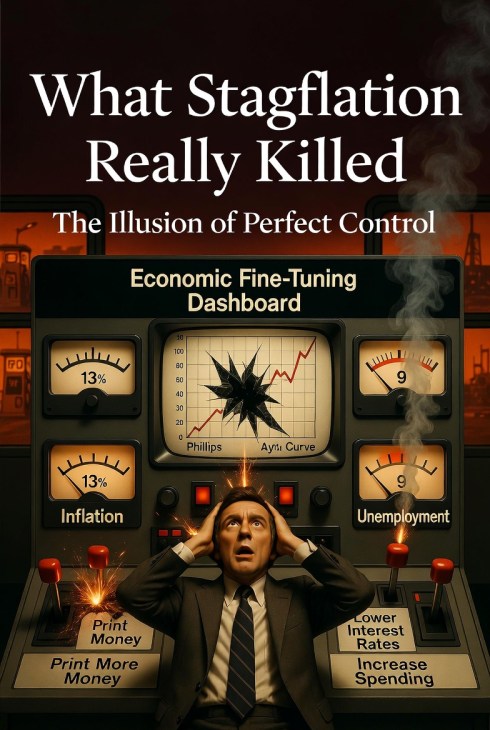

The lesson of 1970s stagflation was not that governments can do nothing. It was that the people running policy understood less than they claimed, and that the tools they trusted were much cruder than advertised. The “Great Inflation” from roughly 1965 to 1982 forced economists and central banks to rethink how inflation, unemployment, and monetary policy actually interact. (Federal Reserve History)

For a time, the postwar consensus rested on a flattering idea. Inflation and unemployment were treated as a manageable trade-off. The Phillips Curve was not just read as a pattern in the data. In practice, it became a governing intuition: if unemployment rose, policymakers could push demand higher and accept somewhat more inflation as the cost. That was the real temptation. A relationship observed under one set of conditions was quietly promoted into an instrument of control. The curve stopped being a caution and became a dashboard. That is where the error entered. As later critiques made clear, any apparent trade-off could break down once expectations adjusted. (Federal Reserve History)

Then the 1970s arrived and the trade-off stopped behaving.

Inflation rose sharply while unemployment also remained painfully high. BLS historical CPI data show annual U.S. inflation at 11.0 percent in 1974, 11.3 percent in 1979, and 13.5 percent in 1980. Federal Reserve History identifies this whole era as the defining macroeconomic crisis of the late twentieth century precisely because it combined persistent inflation with serious economic weakness and forced a rethink of earlier policy assumptions. The old promise had implied that these pressures could be balanced against each other. Instead they arrived together. (Bureau of Labor Statistics)

It is tempting to tell that story too neatly. Some people reduce stagflation to one cause, usually Nixon’s August 1971 suspension of dollar convertibility into gold. That was a major monetary break, and it helped bring the Bretton Woods system to an end. But it was not the whole story. Nixon’s package also included wage and price controls, and the wider period was shaped by multiple interacting forces, including oil shocks and broader inflation dynamics. The point of that complexity is not to rescue the old confidence. It is to bury it. An economy shaped by that many moving parts was never going to be managed with the precision implied by mid-century technocratic rhetoric. (Federal Reserve History)

This is where some critics of monetary manipulation look stronger in retrospect than they did at the time. Austrian economists such as Mises and Hayek had long warned that money and credit are not harmless policy tools. Cheap credit can distort investment. Monetary expansion can scramble price signals. Artificial booms can end in painful correction. There is no need to pretend they possessed a complete script for every feature of 1970s macroeconomics. They did not. But they were directionally right about something central: when policymakers treat money as an instrument of short-run management rather than a framework for stable coordination, they increase the odds of disorder. That warning aged better than the promise of fine-tuning. This is an interpretive judgment, but it is supported by how badly the simpler policy reading of the Phillips Curve fared during the Great Inflation. (Federal Reserve History)

Paul Volcker’s anti-inflation campaign in the early 1980s drove the point home in brutal form. The Federal Reserve’s October 1979 shift to tighter anti-inflation policy helped bring inflation down, but the price of restoring credibility was severe. Federal Reserve History notes that inflation fell sharply after its 1980 peak, while unemployment reached 10.8 percent in late 1982 during the deep 1981–82 recession. That was not the triumph of elegant expert control. It was the bill arriving. Once inflationary disorder hardens, the correction is rarely gentle. (Federal Reserve History)

So what did stagflation actually kill?

Not economics. Not all state action. Not even every Keynesian insight. What it killed was a style of elite confidence. It killed the belief that national economies can be fine-tuned with enough intelligence, enough models, and enough institutional nerve. It killed the conceit that the dashboard is the machine. The language has changed since then. The models are more sophisticated. The temptation is still with us. Every generation of managers wants to believe that this time the controls are better and the uncertainties smaller. The 1970s remain useful because they remind us that policy operates under limits, trade-offs turn ugly, and reality does not care how elegant the model looked on paper. (Federal Reserve History)

Glossary

Phillips Curve

A model associated with a short-run relationship between inflation and unemployment. In practice, many policymakers treated it as if lower unemployment could be purchased with somewhat higher inflation. The 1970s badly damaged confidence in that simple reading. (Federal Reserve History)

Stagflation

A period of high inflation combined with weak growth and high unemployment. The 1970s made the term famous because that combination was supposed to be difficult to sustain under older policy assumptions. (Federal Reserve History)

Fiat money

Money that is not redeemable for a commodity such as gold and instead depends on legal and institutional backing. Nixon’s 1971 decision ended dollar convertibility into gold for foreign governments and central banks. (Federal Reserve History)

Bretton Woods system

The postwar international monetary order in which other currencies were pegged to the U.S. dollar, and the dollar was convertible into gold under the system’s rules. It unraveled in the early 1970s. (Federal Reserve History)

Disinflation

A slowing in the rate of inflation. Prices may still be rising, but less quickly than before. Volcker’s early-1980s policy is a classic U.S. example. (Federal Reserve History)

References / URLs

Federal Reserve History, “The Great Inflation”

https://www.federalreservehistory.org/essays/great-inflation

Federal Reserve History, “Nixon Ends Convertibility of U.S. Dollars to Gold and Announces Wage/Price Controls”

https://www.federalreservehistory.org/essays/gold-convertibility-ends

Federal Reserve History, “Volcker’s Announcement of Anti-Inflation Measures”

https://www.federalreservehistory.org/essays/anti-inflation-measures

Federal Reserve History, “Recession of 1981–82”

https://www.federalreservehistory.org/essays/recession-of-1981-82

Federal Reserve History, “Creation of the Bretton Woods System”

https://www.federalreservehistory.org/essays/bretton-woods-created

U.S. Bureau of Labor Statistics, Historical CPI-U, 1913–2023

https://www.bls.gov/cpi/tables/supplemental-files/historical-cpi-u-202312.pdf

Canada is in the middle of a familiar temptation: the Americans are difficult, therefore the Chinese offer must be sane.

The immediate backdrop is concrete. On January 16, 2026, Canada announced a reset in economic ties with China that includes lowering barriers for a set number of Chinese EVs, while China reduces tariffs on key Canadian exports like canola. (Reuters) Washington responded with open irritation, warning Canada it may regret the move and stressing Chinese EVs will face U.S. barriers. (Reuters)

If you want a simple, pasteable bromide for people losing their minds online, it’s this: the U.S. and China both do bad things, but they do bad things in different ways, at different scales, with different “escape hatches.” One is a democracy with adversarial institutions that sometimes work. The other is a one-party state that treats accountability as a threat.

To make that visible, here are five egregious “hits” from each—then the contrast that actually matters.

Five things the United States does that Canadians have reason to resent

1) Protectionist trade punishment against allies

Steel/aluminum tariffs and recurring lumber duties are the classic pattern: national-interest rhetoric, domestic political payoff, allied collateral damage. Canada has repeatedly challenged U.S. measures on steel/aluminum and softwood lumber. (Global Affairs Canada)

Takeaway: the U.S. will squeeze Canada when it’s convenient—sometimes loudly, sometimes as a bureaucratic grind.

2) Energy and infrastructure whiplash

Keystone XL is the poster child of U.S. policy reversals that impose real costs north of the border and then move on. The project’s termination is documented by the company and Canadian/Alberta sources. (TC Energy)

Takeaway: the U.S. can treat Canadian capital as disposable when U.S. domestic politics flips.

3) Extraterritorial reach into Canadians’ private financial lives

FATCA and related information-sharing arrangements are widely experienced as a sovereignty irritant (and have been litigated in Canada). The Supreme Court of Canada ultimately declined to hear a constitutional challenge in 2023. (STEP)

Takeaway: the U.S. often assumes its laws get to follow people across borders.

4) A surveillance state that had to be restrained after the fact

Bulk telephone metadata collection under Patriot Act authorities became politically toxic and was later reformed/ended under the USA Freedom Act’s structure. (Default)

Takeaway: democracies can drift into overreach; the difference is that overreach can become a scandal, a law change, and a court fight.

5) The post-9/11 stain: indefinite detention and coercive interrogation

Guantánamo’s long-running controversy and the Senate Intelligence Committee’s reporting on the CIA program remain enduring examples of U.S. moral failure. (Senate Select Committee on Intelligence)

Takeaway: the U.S. is capable of serious rights abuses—then also capable of documenting them publicly, litigating them, and partially reversing course.

Five things the People’s Republic of China does that are categorically different

1) Mass rights violations against Uyghurs and other Muslim minorities in Xinjiang

The UN human rights office assessed serious human rights concerns in Xinjiang and noted that the scale of certain detention practices may constitute international crimes, including crimes against humanity. Canada has publicly echoed those concerns in multilateral statements. (OHCHR)

Takeaway: this is not “policy disagreement.” It’s a regime-scale human rights problem.

2) Hong Kong: the model of “one country, one party”

The ongoing use of the national security framework to prosecute prominent pro-democracy figures is a live, observable indicator of how Beijing treats dissent when it has full jurisdiction. (Reuters)

Takeaway: when Beijing says “stability,” it means obedience.

3) Foreign interference and transnational pressure tactics

Canadian public safety materials and parliamentary reporting describe investigations into transnational repression activity and concerns around “overseas police stations” and foreign influence. (Public Safety Canada)

Takeaway: the Chinese state’s threat model can extend into diaspora communities abroad.

4) Systematic acquisition—licit and illicit—of sensitive technology and IP

The U.S. intelligence community’s public threat assessment explicitly describes China’s efforts to accelerate S&T progress through licit and illicit means, including IP acquisition/theft and cyber operations. (Director of National Intelligence)

Takeaway: your “market partner” may also be running an extraction strategy against your innovation base.

5) Environmental and maritime predation at scale

China remains a dominant player in coal buildout even while expanding renewables, a dual-track strategy with global climate implications. (Financial Times)

On the oceans, multiple research and advocacy reports emphasize the size and global footprint of China’s distant-water fishing and associated IUU concerns. (Brookings)

Takeaway: when the state backs extraction, the externalities get exported.

Compare and contrast: the difference is accountability

If you read those lists and conclude “both sides are bad,” you’ve missed the key variable.

The U.S. does bad things in a system with adversarial leak paths:

investigative journalism, courts, opposition parties, congressional reports, and leadership turnover. That doesn’t prevent abuses. It does make abuses contestable—and sometimes reversible. (Senate Select Committee on Intelligence)

China does bad things in a system designed to prevent contestation:

one-party rule, censorship, legal instruments aimed at “subversion,” and a governance style that treats independent scrutiny as hostile action. The problem isn’t “China is foreign.” The problem is that the regime’s incentives run against transparency by design. (Reuters)

So when someone says, “Maybe we should pivot away from the Americans,” the adult response is:

- Yes, diversify.

- No, don’t pretend dependency on an authoritarian state is merely a swap of suppliers.

A quick media-literacy rule for your feed

If a post uses a checklist like “America did X, therefore China is fine,” it’s usually laundering a conclusion.

A better frame is risk profile:

- In a democracy, policy risk is high but visible—and the country can change its mind in public.

- In a one-party state, policy risk is lower until it isn’t—and then you discover the rules were never meant to protect you.

Canada can do business with anyone. But it should not confuse trade with trust, or frustration with Washington with safety in Beijing.

If Canada wants autonomy, the answer isn’t romanticizing China. It’s building a broader portfolio across countries where the rule of law is not a slogan in a press release.

References

- Canada–China trade reset (EV tariffs/canola): Reuters; Guardian. (Reuters)

- U.S. criticism of Canada opening to Chinese EVs: Reuters. (Reuters)

- U.S. tariffs/lumber disputes: Global Affairs Canada; Reuters. (Global Affairs Canada)

- Keystone XL termination: TC Energy; Government of Alberta. (TC Energy)

- FATCA Canadian challenge result: STEP (re Supreme Court dismissal). (STEP)

- USA Freedom Act / end of bulk metadata: Lawfare; Just Security. (Default)

- CIA detention/interrogation report: U.S. Senate Intelligence Committee report PDF. (Senate Select Committee on Intelligence)

- Guantánamo context: Reuters; Amnesty. (Reuters)

- Xinjiang assessment: OHCHR report + Canada multilateral statement. (OHCHR)

- Hong Kong NSL crackdown example: Reuters (Jimmy Lai). (Reuters)

- Transnational repression / overseas police station concerns: Public Safety Canada; House of Commons report PDF. (Public Safety Canada)

- China tech acquisition / IP theft framing: ODNI Annual Threat Assessment PDF. (Director of National Intelligence)

- Coal buildout: Financial Times; Reuters analysis. (Financial Times)

- Distant-water fishing footprint / IUU concerns: Brookings; EJF; Oceana. (Brookings)

In recent years, Venezuela was often held up as a shining example by some Western socialists as the ultimate proof that their economic model could create a fairer society. Big names on the left, from Jeremy Corbyn to Bernie Sanders, once praised Venezuela as a socialist success story.

But when the country’s economy collapsed, when its people faced hunger, and when millions fled, those same voices grew notably quiet. Today, the narrative has shifted. Supporters who once looked to Venezuela now point to Nordic countries, distancing themselves from what they once endorsed.

The reality is that Venezuela’s tragic decline serves as a cautionary tale. It shows that simply promising “free stuff” and wealth redistribution doesn’t automatically lead to prosperity. Instead, it can lead to economic dysfunction and suffering.

In this post, we’ve unpacked how the once-celebrated Venezuelan model has become an uncomfortable silence among its former admirers. We’ve seen how the economic realities and human suffering in Venezuela stand in stark contrast to the optimistic promises of socialism. And as we look at these lessons, it’s clear that Western societies need to reevaluate the ideologies we champion. Ultimately, if we want to build fairer and more prosperous societies, we need to be honest about what works and what doesn’t, and not shy away from these tough conversations.

First, from the Manhattan Institute, there’s an analysis by Daniel Di Martino arguing that Venezuela’s crisis was primarily caused by socialist policies like nationalizations and price controls.

Second, the Fraser Institute provides a historical perspective from Fred McMahon, who notes that Venezuela’s decline started with economic mismanagement even before the full rise of socialist policies.

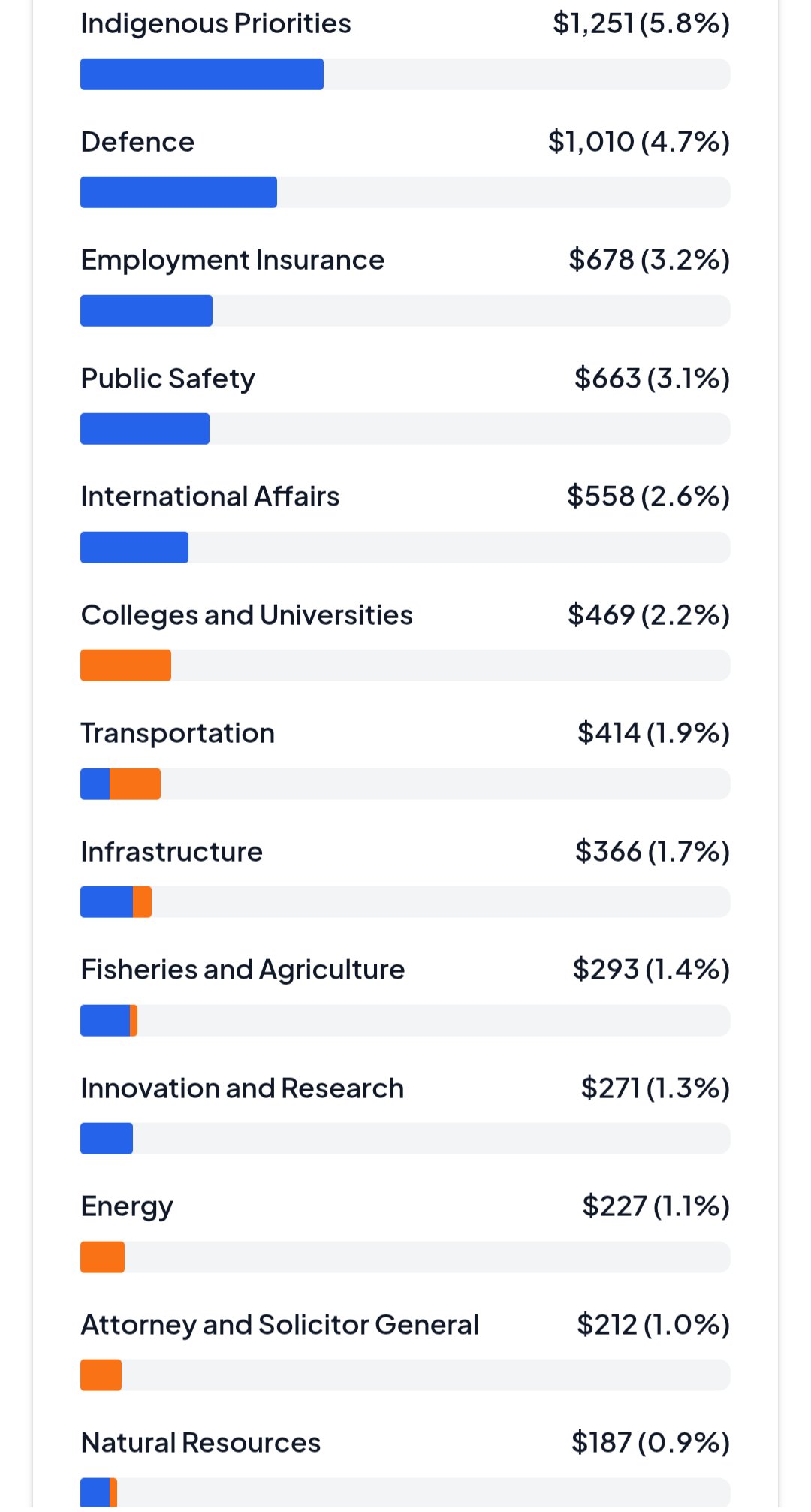

Canada’s federal budget tells a story that few seem willing to read critically. According to CanadaSpends.com, Ottawa allocates $1.251 billion—5.8 percent of the budget—to “Indigenous Priorities,” eclipsing even Defence ($1.010 billion, 4.7 percent). The arithmetic alone invites scrutiny. At what point does reconciliation become a fiscal reflex, untethered from measurable outcomes?

The Arithmetic of Imbalance

Consider a simple exercise in opportunity cost. Halving “Indigenous Priorities” to $625.5 million would free an equal amount—$625.5 million—for redeployment elsewhere. Redirecting that sum to Public Safety, currently $663 million (3.1 percent), would nearly double its capacity to $1.288 billion. The outcome: stronger policing resources, reinforced border security, and potentially measurable reductions in crime—objectives grounded in deterrence rather than symbolism.

This is not an argument against Indigenous advancement. It is an argument for proportionality and accountability. “Indigenous Priorities” now consume more than Employment Insurance ($678 million), International Affairs ($558 million), and Colleges and Universities ($469 million) combined. Defence, tasked with national sovereignty, trails by $241 million. When cultural or consultative programs eclipse citizen security and education, something in our fiscal compass is misaligned.

The Accountability Deficit

Proponents will cite historical redress, and that moral claim has force. But truth in budgeting requires evidence, not sentiment. Where are the audited outcomes showing that each billion spent yields measurable gains in Indigenous health, education, or economic independence?

The problem is not merely bureaucratic inertia—it is structural opacity, worsened by political choice. In December 2015, the newly elected Liberal government suspended enforcement of the First Nations Financial Transparency Act, which had required Indigenous governments to publish audited financial statements and leadership salaries. The minister at the time, Carolyn Bennett, directed her department to “cease all discretionary compliance measures” and reinstated funding to communities that refused disclosure.

In effect, Ottawa dismantled the only system ensuring public visibility into how billions of tax dollars are spent. Nearly a decade later, the Auditor General’s 2025 report found “unsatisfactory progress” on more than half of all Indigenous-services audit recommendations, despite an 84 percent increase in program spending since 2019. The data are undeniable: accountability has eroded even as expenditures have soared.

Fiscal Compassion, Not Fiscal Indulgence

Canada does not need less compassion; it needs measurable compassion—spending that demonstrably improves lives rather than perpetuates dependency. Halving the current Indigenous Priorities budget would not abolish support or reverse reconciliation. It would introduce accountability, allowing funds to be reallocated to public safety, infrastructure, or innovation—areas with immediate and empirically verifiable benefits.

Until Indigenous programs are evaluated with the same rigour applied to defence, education, or social insurance, billion-dollar gestures will remain ends in themselves—virtue without verification.

References

- CanadaSpends.com – Federal Tax Visualizer

- Government of Canada Statement on the First Nations Financial Transparency Act (2015)

- Office of the Auditor General of Canada, 2025 Report – Programs for First Nations

- Canadian Affairs News – Poll: Canadians Want Transparency in First Nations Finances (2025)

- Standing Committee Appearance: Supplementary Estimates (2024)

- Crown-Indigenous Relations and Northern Affairs Canada 2023–24 Results Report

Poland’s ascent to a $1 trillion economy in September 2025 marks a remarkable transformation. Emerging from the wreckage of Soviet control, Poland has become one of Europe’s fastest-growing economies over the past three decades. With GDP growth projected at 3.2 percent for 2025, unemployment near 3 percent (harmonized), and inflation moderating to 2.8 percent in August, it demonstrates resilience and steady progress.

Canada, with a nominal GDP of roughly $2.39 trillion, is richer in absolute terms but faces weaker dynamics: growth forecasts of just 1.2 percent, unemployment climbing to 7.1 percent in August, and persistent concerns over productivity and rising public debt. The contrast raises an important question: which elements of Poland’s success can Canada responsibly adapt to its own very different circumstances?

1. Manufacturing Capacity and Industrial Resilience

Poland’s economy has benefited from retaining a strong industrial base, especially in automotive, machinery, and technology supply chains closely integrated with Germany. This foundation has provided steady export growth and employment, while limiting excessive reliance on fragile overseas supply chains.

Canada, by contrast, has seen its manufacturing share of GDP shrink over decades as industries relocated or hollowed out. While Canada cannot replicate Poland’s role as a mid-cost hub inside the EU, it could adapt the principle: incentivize the repatriation or expansion of high-value sectors (e.g., EV manufacturing, critical minerals processing, aerospace). Strategic tax credits, infrastructure investment, and streamlined permitting could restore resilience and provide middle-class employment.

Lesson for Canada: industrial renewal need not mean autarky, but building domestic capacity in key sectors reduces vulnerability to shocks — as Poland’s stability during recent European crises shows.

2. Immigration Policy and Integration Capacity

Poland has pursued a relatively selective immigration system, prioritizing labor market fit and manageable inflows. While Poland remains relatively homogeneous (Eurostat estimates about 98% ethnic Polish in 2022), its policy has focused on ensuring newcomers integrate into economic and cultural life. The result has been high employment among migrants and limited social disruption compared with some Western European peers.

Canada, by contrast, accepts large inflows — even after scaling back targets to 395,000 permanent residents in 2025 — and faces housing pressures and uneven integration outcomes. Canada’s homicide rate (2.27 per 100,000 in 2022) is higher than Poland’s (0.68), though crime is shaped by many factors beyond immigration. Still, rapid population growth without infrastructure, housing, and language capacity has heightened social strains.

Lesson for Canada: immigration policy should balance humanitarian goals with absorptive capacity. Emphasizing labor alignment, regional settlement, and language proficiency — as Poland has done — would help ensure inflows strengthen productivity while minimizing stress on housing and services.

3. Cultural Continuity and Heritage as Assets

Poland has paired modernization with deliberate protection of its cultural identity. The restoration of Kraków and Warsaw not only preserves heritage but fuels a thriving tourism sector. National traditions, rooted in Catholicism for many Poles, have also informed family policy (e.g., child benefits) and provided a sense of cohesion during rapid economic change.

Canada’s pluralism differs fundamentally, and it cannot — and should not — mimic Poland’s religious or cultural model. Yet Canada can still learn from the broader principle: treating heritage and shared narratives as economic and social assets rather than obstacles. Investments in Indigenous landmarks, Francophone culture, and historic architecture could enrich tourism, foster pride, and strengthen cohesion. Likewise, family-supportive policies (parental leave, child benefits, flexible work arrangements) are essential as Canada faces declining fertility and an aging workforce.

Lesson for Canada: cultural preservation and demographic support are not nostalgic luxuries — they can reinforce economic stability and social cohesion.

4. Fiscal Prudence and Monetary Autonomy

Poland’s choice to retain the zloty rather than adopt the euro preserved monetary flexibility. Combined with relatively conservative fiscal policies (public debt at about 49% of GDP in 2024, well below EU ceilings), this has allowed Poland to respond to crises with agility while maintaining competitiveness.

Canada already benefits from its own currency, but fiscal expansion has pushed federal debt above 65% of GDP. While Canada’s wealth affords greater borrowing room, long-term sustainability requires discipline. Poland’s experience suggests that debt caps, counter-cyclical saving, and careful monetary coordination can preserve resilience without stifling growth.

Lesson for Canada: fiscal credibility is itself an economic asset. Setting clearer debt-to-GDP targets and enforcing discipline would strengthen Canada’s ability to weather global volatility.

Conclusion

Poland’s trajectory is not without challenges. It faces demographic decline, reliance on EU subsidies, and governance controversies that Canada would not wish to replicate. But its achievements underscore a vital truth: prosperity need not mean sacrificing resilience, identity, or cohesion.

For Canada, the actionable lessons are clear:

-

rebuild key industries,

-

align immigration with integration capacity,

-

invest in heritage and families,

-

and re-anchor fiscal policy in prudence.

Adapted to Canadian realities, these reforms could help lift growth closer to 3 percent, reduce unemployment, and restore a sense of national momentum.

References

-

International Monetary Fund (IMF). World Economic Outlook Database, October 2025.

-

Statistics Canada. Labour Force Survey, August 2025.

-

Eurostat. Population Structure and Migration Statistics, 2022–2025.

-

OECD. Economic Outlook: Poland and Canada, 2025.

-

World Bank. World Development Indicators, 2024–2025.

-

UN Office on Drugs and Crime (UNODC). Global Homicide Statistics, 2022.

-

National Bank of Poland. Annual Report, 2024.

-

Government of Canada. Immigration Levels Plan 2025–2027.

When a government spends beyond its means, citizens eventually pay the price. This reality looms over Prime Minister Marc Carney’s fiscal approach, which has drawn mounting criticism for being both irresponsible and inflationary. With federal spending ballooning under his leadership, Canada faces mounting deficits that risk fueling long-term inflation and undermining economic stability.

At its core, Carney’s fiscal strategy rests on aggressive public expenditure with the stated aim of stimulating growth and addressing social inequities. While such intentions may sound noble, the result is the same problem that has plagued countless governments before: spending outstrips revenue, and deficits grow. Canada is already burdened with significant debt from past administrations, and Carney’s unwillingness to rein in spending threatens to push the nation further into the red. This raises serious concerns about the sustainability of his policies.

The inflationary risks cannot be overstated. When governments flood the economy with borrowed money, demand rises artificially, often faster than supply can keep up. The outcome is predictable: rising prices that erode the purchasing power of ordinary Canadians. Carney’s background as a central banker makes his freewheeling fiscal approach especially puzzling, given that he fully understands how unchecked deficits translate into inflationary pressures. By ignoring these basic economic principles, he risks not only undermining Canadian competitiveness but also hollowing out the middle class he claims to champion.

The consequences of such policies ripple outward. Inflation means higher food and housing costs, disproportionately hurting working families. Higher deficits translate into heavier debt servicing, which steals resources from essential services like healthcare and infrastructure. In short, Carney’s fiscal vision looks less like a plan for prosperity and more like a reckless gamble with the nation’s future.

Table: Why Carney’s Fiscal Policies Risk Inflation

| Policy/Action | Short-Term Effect | Long-Term Risk |

|---|---|---|

| Aggressive public spending | Temporary economic stimulus | Rising deficits and debt burden |

| Borrowing to finance programs | Increased demand | Inflationary pressure and weakened currency |

| Ignoring fiscal restraint | Boosts political popularity | Erodes economic competitiveness |

| Large deficits | Expanded government footprint | Reduced fiscal flexibility in future crises |

| Reliance on debt-financed growth | Superficial prosperity | Declining middle-class purchasing power |

References

- Canada’s Budget Deficit First Four Months 2025/26 — Between April-July 2025 the federal deficit rose to C$7.79 billion, as spending grew faster (3.0%) than revenues (1.6%). (Reuters)

- Deficit Estimate for Entire Fiscal Year — Economists project Canada’s 2025-26 deficit could hit C$70 billion, more than the previous year’s (approx. C$48 billion). (TT News)

- Government Spending Rise — 2025-26 federal main estimates show total spending of C$486.9 billion, an 8.4% increase from the previous year. (iPolitics)

- Projected Future Deficits — Carney’s platform projects yearly deficits of ~C$62 billion in 2025-26, dropping gradually in following years but still significant. (Taxpayer)

- Deficit Pressure from Trade War & Tariffs — U.S. tariffs and counter-tariffs affecting revenues and costs are cited as one factor expected to increase deficits well above initial forecasts. (The Hub)

- Official Signalling of Higher Deficit — Ottawa has publicly acknowledged that the upcoming budget will feature a “substantial” deficit, larger than last year’s, and has warned that all departments must participate in spending restraint efforts. (Global News)

Your opinions…