You are currently browsing the tag archive for the ‘Inflation’ tag.

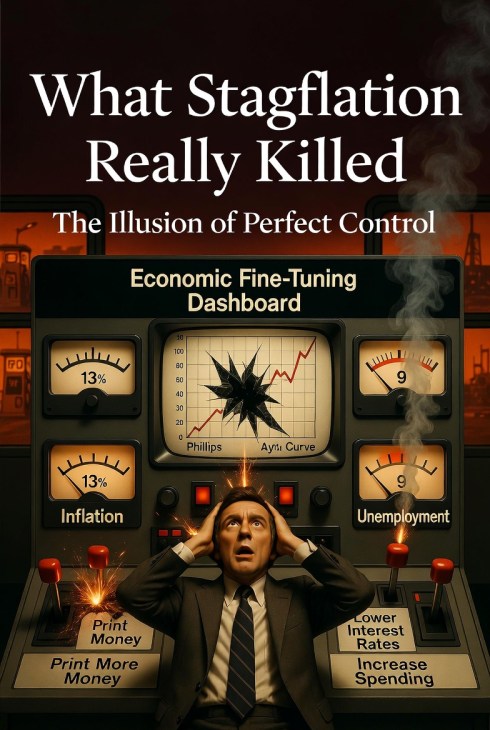

The lesson of 1970s stagflation was not that governments can do nothing. It was that the people running policy understood less than they claimed, and that the tools they trusted were much cruder than advertised. The “Great Inflation” from roughly 1965 to 1982 forced economists and central banks to rethink how inflation, unemployment, and monetary policy actually interact. (Federal Reserve History)

For a time, the postwar consensus rested on a flattering idea. Inflation and unemployment were treated as a manageable trade-off. The Phillips Curve was not just read as a pattern in the data. In practice, it became a governing intuition: if unemployment rose, policymakers could push demand higher and accept somewhat more inflation as the cost. That was the real temptation. A relationship observed under one set of conditions was quietly promoted into an instrument of control. The curve stopped being a caution and became a dashboard. That is where the error entered. As later critiques made clear, any apparent trade-off could break down once expectations adjusted. (Federal Reserve History)

Then the 1970s arrived and the trade-off stopped behaving.

Inflation rose sharply while unemployment also remained painfully high. BLS historical CPI data show annual U.S. inflation at 11.0 percent in 1974, 11.3 percent in 1979, and 13.5 percent in 1980. Federal Reserve History identifies this whole era as the defining macroeconomic crisis of the late twentieth century precisely because it combined persistent inflation with serious economic weakness and forced a rethink of earlier policy assumptions. The old promise had implied that these pressures could be balanced against each other. Instead they arrived together. (Bureau of Labor Statistics)

It is tempting to tell that story too neatly. Some people reduce stagflation to one cause, usually Nixon’s August 1971 suspension of dollar convertibility into gold. That was a major monetary break, and it helped bring the Bretton Woods system to an end. But it was not the whole story. Nixon’s package also included wage and price controls, and the wider period was shaped by multiple interacting forces, including oil shocks and broader inflation dynamics. The point of that complexity is not to rescue the old confidence. It is to bury it. An economy shaped by that many moving parts was never going to be managed with the precision implied by mid-century technocratic rhetoric. (Federal Reserve History)

This is where some critics of monetary manipulation look stronger in retrospect than they did at the time. Austrian economists such as Mises and Hayek had long warned that money and credit are not harmless policy tools. Cheap credit can distort investment. Monetary expansion can scramble price signals. Artificial booms can end in painful correction. There is no need to pretend they possessed a complete script for every feature of 1970s macroeconomics. They did not. But they were directionally right about something central: when policymakers treat money as an instrument of short-run management rather than a framework for stable coordination, they increase the odds of disorder. That warning aged better than the promise of fine-tuning. This is an interpretive judgment, but it is supported by how badly the simpler policy reading of the Phillips Curve fared during the Great Inflation. (Federal Reserve History)

Paul Volcker’s anti-inflation campaign in the early 1980s drove the point home in brutal form. The Federal Reserve’s October 1979 shift to tighter anti-inflation policy helped bring inflation down, but the price of restoring credibility was severe. Federal Reserve History notes that inflation fell sharply after its 1980 peak, while unemployment reached 10.8 percent in late 1982 during the deep 1981–82 recession. That was not the triumph of elegant expert control. It was the bill arriving. Once inflationary disorder hardens, the correction is rarely gentle. (Federal Reserve History)

So what did stagflation actually kill?

Not economics. Not all state action. Not even every Keynesian insight. What it killed was a style of elite confidence. It killed the belief that national economies can be fine-tuned with enough intelligence, enough models, and enough institutional nerve. It killed the conceit that the dashboard is the machine. The language has changed since then. The models are more sophisticated. The temptation is still with us. Every generation of managers wants to believe that this time the controls are better and the uncertainties smaller. The 1970s remain useful because they remind us that policy operates under limits, trade-offs turn ugly, and reality does not care how elegant the model looked on paper. (Federal Reserve History)

Glossary

Phillips Curve

A model associated with a short-run relationship between inflation and unemployment. In practice, many policymakers treated it as if lower unemployment could be purchased with somewhat higher inflation. The 1970s badly damaged confidence in that simple reading. (Federal Reserve History)

Stagflation

A period of high inflation combined with weak growth and high unemployment. The 1970s made the term famous because that combination was supposed to be difficult to sustain under older policy assumptions. (Federal Reserve History)

Fiat money

Money that is not redeemable for a commodity such as gold and instead depends on legal and institutional backing. Nixon’s 1971 decision ended dollar convertibility into gold for foreign governments and central banks. (Federal Reserve History)

Bretton Woods system

The postwar international monetary order in which other currencies were pegged to the U.S. dollar, and the dollar was convertible into gold under the system’s rules. It unraveled in the early 1970s. (Federal Reserve History)

Disinflation

A slowing in the rate of inflation. Prices may still be rising, but less quickly than before. Volcker’s early-1980s policy is a classic U.S. example. (Federal Reserve History)

References / URLs

Federal Reserve History, “The Great Inflation”

https://www.federalreservehistory.org/essays/great-inflation

Federal Reserve History, “Nixon Ends Convertibility of U.S. Dollars to Gold and Announces Wage/Price Controls”

https://www.federalreservehistory.org/essays/gold-convertibility-ends

Federal Reserve History, “Volcker’s Announcement of Anti-Inflation Measures”

https://www.federalreservehistory.org/essays/anti-inflation-measures

Federal Reserve History, “Recession of 1981–82”

https://www.federalreservehistory.org/essays/recession-of-1981-82

Federal Reserve History, “Creation of the Bretton Woods System”

https://www.federalreservehistory.org/essays/bretton-woods-created

U.S. Bureau of Labor Statistics, Historical CPI-U, 1913–2023

https://www.bls.gov/cpi/tables/supplemental-files/historical-cpi-u-202312.pdf

Inflation is the steady climb in prices for goods and services, shrinking what your money can buy over time. It arises when too much money chases too few goods, a dynamic fueled by policy missteps and economic shocks. This essay examines inflation’s primary drivers, emphasizing government spending and money printing, with a focus on Canadian examples, including recent actions, grounded in hard evidence. The stakes are high: inflation corrodes savings, disrupts planning, and frays societal unity, demanding a clear-eyed look at its causes.

Government spending, especially when deficit-financed, is a key inflationary culprit. Large-scale fiscal interventions—like Canada’s $500 billion in COVID-19 relief programs in 2020–2021, including the Canada Emergency Response Benefit (CERB)—flooded the economy with cash, spiking demand. This surge, coupled with supply constraints, drove Canada’s inflation to 8.1% in June 2022, a 40-year high. A 2022 Scotiabank analysis estimated these programs added 0.45 percentage points to core inflation by widening the output gap. Historically, Canada’s 1970s deficit spending, which fueled double-digit inflation, mirrors this pattern. Recent policies, such as 2025 provincial and federal inflation-relief transfers, risk further stoking demand, with Scotiabank projecting they could necessitate a 38% share of the Bank of Canada’s rate hikes to counteract their inflationary impulse.

Money printing, through central bank policies like quantitative easing, devalues currency by expanding the money supply. In Canada, the Bank of Canada’s purchase of $400 billion in government bonds during 2020–2021 lowered interest rates to 0.25%, encouraging spending but devaluing the Canadian dollar. This imported inflation, as a weaker dollar raised import costs, contributing over 50% to inflation in final domestic demand by late 2022. Zimbabwe’s hyperinflation in the 2000s, peaking at 79.6 billion percent monthly, offers an extreme parallel, driven by unchecked money creation. In 2024, the Bank of Canada’s continued quantitative tightening, alongside a 2025 policy rate hold at 4.5%, reflects efforts to curb these pressures, though global factors like U.S. inflation still amplify Canada’s import-driven price hikes.

Supply shocks and wage-price spirals further aggravate inflation. Canada’s 2022 supply chain disruptions, exacerbated by global port delays and China’s COVID-zero policy, spiked food and energy prices—food alone contributed 1.02 percentage points to inflation. The 1973 OPEC embargo, which quadrupled oil prices, offers a historical parallel, as does Canada’s 2022 experience with Russia’s invasion of Ukraine, which drove gasoline prices to $2 per liter. Wage-price spirals, fueled by 4.5% wage growth in advanced economies in 2021, also played a role, with Canada’s labor shortages post-reopening pushing service prices up 5% by mid-2022. Current U.S. tariffs on Canadian goods, as of January 2025, threaten to raise import costs further, with uncertain pass-through to consumers, potentially sustaining inflationary pressure.

Inflation’s corrosive grip—evident in Canada’s 2022 peak and lingering 2.6% rate in February 2025—demands accountability. Government spending and money printing, as seen in Canada’s pandemic policies and bond purchases, are potent drivers, amplified by supply shocks and wage dynamics. Historical and recent evidence, from 1970s deficits to 2025 tariff risks, underscores the need for disciplined fiscal and monetary policy. Citizens must demand restraint to protect purchasing power and preserve economic stability before inflation’s tide engulfs us all.

Bibliography

- Congressional Budget Office. (1980). The Economic Effects of Federal Deficits. https://www.cbo.gov/publication/21925

- Energy Information Administration. (1974). Historical Overview of the 1973 Oil Crisis. https://www.eia.gov/history/

- European Central Bank. (2019). Asset Purchase Programmes. https://www.ecb.europa.eu/mopo/implement/omt/html/index.en.html

- Federal Reserve Bank of San Francisco. (2021). Fiscal Policy and Excess Inflation During the Pandemic. https://www.frbsf.org/economic-research/publications/economic-letter/2021/may/fiscal-policy-and-excess-inflation-during-pandemic/

- International Monetary Fund. (2009). Zimbabwe: Hyperinflation. https://www.imf.org/en/Publications/WP/Issues/2016/12/31/Zimbabwe-Hyperinflation-22603

- OECD. (2022). Employment Outlook 2022. https://www.oecd.org/economy/employment-outlook/

- Scotiabank. (2022). Canadian Inflation: Mostly Temporary and Foreign, But Pandemic Programs Have a Major Impact on Policy Rates. https://www.scotiabank.com

- Statistics Canada. (2024). High Inflation in 2022 in Canada: Demand–Pull or Supply–Push?. https://www150.statcan.gc.ca

- The Globe and Mail. (2022). The Most Important Source of Canada’s Inflation: The Government Borrowed More Than $700-Billion. https://www.theglobeandmail.com

I think I’ve looked up and had explained to me what the term “inflation” is. The concept has remained a bit of a mystery. Mark Blyth the Scottish-American (Austerity – The History of a Dangerous Idea) economist parsed down the meaning of inflation to this – “too much money chasing not enough goods in an economy”. I like that definition as it sticks easily in the mind. However, without the necessary context, understanding what inflation is remains elusive.

Enter Yanis Varoufakis and his book “Talking to My Daughter About the Economy or, How Capitalism Works – and How it Fails”. This short quote describes how inflation and deflationary pressures work in an economy – he tells a story based on a famous paper by R.A. Radford titled The Economic Organization of a P.O.W. camp (original linked here).

“The Exchange Value of Money

When I was your age I recall hearing a grown-up saying something I could not get my head around. I just did not get it, however hard I tried. Even when I thought I had understood it, I tried to explain it to a friend and realized that I hadn’t. What was it that this grown-up had said? That a one-thousand-drachma note (the currency we had then) cost only twenty drachmas to produce. How can it be worth a thousand dratchmas, I kept wondering, when it only cost twenty.

Maybe you are smarter than I was, but humour me nevertheless as I attempt to explain this puzzle in the context of Radford’s POW camp. Periodically, the Red Cross Would place a few more cigarettes in the prisoners’ packages but keep the quantity of chocolate, tea, and coffee the same. When extra cigarettes arrived, each cigarette now bought less coffee, less chocolate, and less tea.

Why?

Since overall a larger number of cigarettes now corresponded to the same amount coffee and tea, each individual cigarette corresponded to less coffee and less tea. The opposite also held true: the fewer cigarettes there were in comparison to the other goods that the Red Cross placed in the packages, the great the exchange value, or purchasing power, of each cigarette. In short, the purchasing power of a unit of currency has nothing to do with how much it costs to produce but, rather, its relative abundance or scarcity.

Imagine that a prisoner has been hoarding his cigarettes in order to make a large purchase when suddenly the Red Cross sends tons of cigarettes to the captives. Suddenly, the exchange value or his cigarettes drops, and his parsimony and abstinence have been to no avail.

In this way we see how having access to a currency lubricates transactions to no end, helping the economy move more commodities more quickly. On the other hand, for a currency to function it requires trust and faith: the trust that everyone will continue to accept it in return for any commodity, which is in turn based on faith that the currency’s exchange value will be maintained. It is no coincidence that in your second language, Greek, the word for “coin: (nomisma) straddles the verb “to think” (nomizo) and the noun for “law” (nomos). Indeed, what gives value to coins and paper money is the legal obligation to accept them across the realm and the belief that they are and will remain valuable.

One night Allied Bombers hammered the area where the camp was located. The bombs landed closer and closer, some falling in the camp itself. All night long the prisoners wondered whether they would live to see daybreak. The next day the exchange value of cigarettes had gone through the roof! Why? Because over the course of that endless night, surrounded by exploding bombs and consumed by anxiety, the prisoners had smoked cigarette after cigarette. In the morning the total number of cigarettes had shrunk dramatically in relation to the other goods. If previously five cigarettes had been needed to buy one chocolate bar, now only one cigarette was needed to buy that same bar.

In short, the bombardment had caused what is known as price deflation – a decrease in all prices as a result of a reduction of the quantity of money in relation to all other goods. The opposite, a genderal increase in prices as a larger quantity of money in the overall system, is known as price inflation.”

–Talking to My Daughter About the Economy or, How Capitalism Works – and How It Fails. Yanis Varoufakis, pp 142 -144.

So, this is how I increased my knowledge of basic economic theory and what I think is a great heuristic tool if you happen to be trying to explain what inflation is and how it works in an economy. I will need to reread both Blyth’s ( his writing is for the layperson but remains quite dense and meaty, a slow but rewarding go) and Varoufakis’s books again as both were invaluable to understand how our economy works.

Your opinions…